A while back, I wrote an article about tax auditors not knowing your business. In today’s post, we will look at the CRA’s appeal department’s knowledge of the restaurant business. I wish I could say that Appeals Officers are better equipped to deal with restaurant tax audit issues, but I can’t. Continue reading “CRA Appeals Officers Don’t Know Your Business”

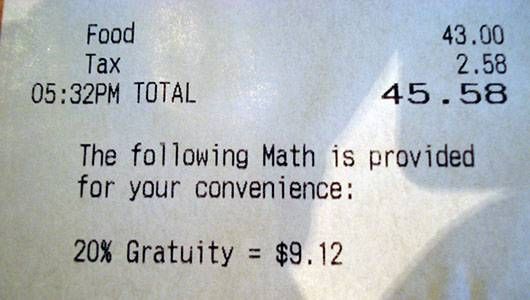

More on the Taxation of Tips

A little while back, I was the main source for an article in a Globe and Mail about the taxation of tips in Canada. I’ve written about taxing tips before, here and here. In this post, I’ll give an update and discuss two problem areas that most restaurateurs need to know about. Continue reading “More on the Taxation of Tips”

Another Tax Appeal Home Run

A restaurateur approached me just after he had received notice that his bar was going to be reassessed for HST on unreported sales. This was a fairly typical situation that many bar and restaurants find themselves in after an audit. There is always a way to “fight” or appeal these cases, at least in part. So, I took the case. Continue reading “Another Tax Appeal Home Run”

Percentage Discounts

A few months ago, Dining Date Night began offering customers a 30% discount at various restaurants in Toronto. In order to get the discount, a customer books a reservation on a website and pays a $10 fee to Dining Date Night. When the customer visits the restaurant, 30% of the total bill (before taxes) is deducted as a discount. This type of promotion is relatively good for both the consumer and the restaurant that provides the discount, because the restaurant can restrict the hours when reservations may be taken.

Groupon Taxes

I’ve written a couple of articles about Groupon on my sister blog, Canadian Restaurateur. This is part of a series that will cover accounting for Groupon certificates, setting up your Point of Sale (POS) system to properly track coupons and discounts, using QuickBooks to enter Groupon transactions, examining the tax treatment of Groupon certificates (this one), and finally, determining whether your restaurant should consider Groupon.

Proving Automobile Business Use

Many restaurant owners use their automobiles for picking up supplies for the business, researching other restaurants, and making trips related to the restaurant’s operations. In Canada, individuals are able to claim a reasonable portion of their automobile expenses against their employment income from the business. Even if you don’t draw a salary, you’re still considered an employee, by being a director of the company.

Beware Harried Ontario Tax Auditors!

When the Ontario government repealed the Retail Sales Tax (RST) in favour of the new Harmonized Sales Tax (HST), it transferred audit and collection activities to the Canada Revenue Agency. Unfortunately, that doesn’t mean Ontario restaurants can forget about the old RST!

Ontario is still responsible for auditing the old RST for periods up to June 30, 2010. Under the Statute of Limitations, Ontario has up to four years to audit the RST. Actually, they can go back more than four years, if they can show fraud or misrepresentation or if they obtain a waiver from the taxpayer.

Many of these Ontario auditors will be transferring to the CRA in 2012. So, they are racing to complete audits of most Ontario RST vendors. This is especially true for Ontario restaurants, which have always been a target of the Ministry of Revenue.

Taxing Theft

We all know that some amount of alcohol will be pilfered. Don’t you love that word? Pilfered. Sounds like a mere pittance. It is anything but. As a rule of thumb, the cost of the theft will be about three times the cost of the alcohol that is, ah, pilfered.

If you’ve been following recent posts on my sister blog, Canadian Restaurateur, you may have noticed a theme. Theft. All restaurateurs know that theft is a significant issue that requires our constant vigilance. The cost of the stolen product is bad enough, but if you also have to pay tax (plus penalties and interest) on the retail value of the stolen product, it becomes a huge issue. Everyone knows it isn’t right that a restaurateur should have to pay tax “as if” the stolen alcohol had been sold. Unfortunately, that isn’t the way it works in most tax jurisdictions.

Perfect Pour = Unreported Sales (and Taxes)?

Huh? Do you mean that if I never over-pour drinks, my establishment can still be accused of under-reporting my sales (and taxes) during an audit? That can’t be right! Can it? Unfortunately, it IS true for almost every restaurant and bar in Canada! Today’s post explains how this happens and what you can do about it.

Most restaurants and bars use shot glasses or portion control pourers to accurately measure the amount of liquor that goes into cocktails, mixed drinks and shots. Meticulously training bartenders and monitoring pouring, you’re fairly confident that your pouring is fairly accurate, if not “perfect”. Even if it is, your establishment will be over-pouring all of your liquor drinks by at least 4%!

Why?

Continue reading “Perfect Pour = Unreported Sales (and Taxes)?”

CRFA Publishes Licensee Pricing Calculators Using The New HST

Recently, the Canadian Restaurant and Foodservices Association (CRFA) published three calculators to help restaurateurs determine the effect on the new HST, effective July 1, 2010, on their prices. The calculators cover wine, spirits and beer. I’ve included the links, below. You can read more and find a discussion on their use and potential effects on your menu pricing in July, here.