A little while back, I was the main source for an article in a Globe and Mail about the taxation of tips in Canada. I’ve written about taxing tips before, here and here. In this post, I’ll give an update and discuss two problem areas that most restaurateurs need to know about.

The less you control tips, the better.

At the time of writing this post, there are two types of tips: “controlled” and “direct“. Tips are controlled where management gets involved with the allocation of tips to servers and other staff members. Direct tips are those that go straight from the customer to the server. Credit and debit card tips that are passed through to the server who earned them are also considered “direct”.

The CRA considers direct tips to be earned by the employee receiving them. They are not subject to CPP or EI withholdings by the employer and they are not included on employee T4 slips. It is up to the employee to declare tips earned and report them on their annual income tax returns.

Controlled tips, however, are considered to be income of the restaurant and subject to HST. Where management takes an active role in divvying up tips among members, the CRA will consider these tips to be controlled.

Two common situations can result in severe tax implications for many bar and restaurant owners. Tip pooling and automatic gratuities. Let’s discuss these.

Tip Pooling

Many restaurants employ a tip pool as a means to ensure that everyone is aware of customer service, even when it does not concern “their” customers. Some restaurants reallocate some of the tip pool to non-servers, such as dishwashers, bussers, host/hostesses and kitchen staff. Unfortunately, when management decides who gets what, the tips in the tip pool are very likely to be considered controlled.

When this happens, the tips are considered to be income of the restaurant. The restaurant should have charged HST (but didn’t). This creates a very significant potential liability, should the CRA choose your restaurant for an audit. Fortunately, the restaurant can get a deduction for tips paid out to its employees. But the restaurant must be able to prove the payments were made. One other unfortunate implication of this is that the restaurant must include these payments on the employees’ T4s and make withholdings for CPP and EI. Your servers are going to love you for this.

If you want the benefits of tip pooling without the problem of having management control, you will have to get a bit creative. I have advised several clients on the correct procedures to employ that will help ensure pooled tips are still considered “direct” in the eyes of the CRA.

Automatic Gratuities

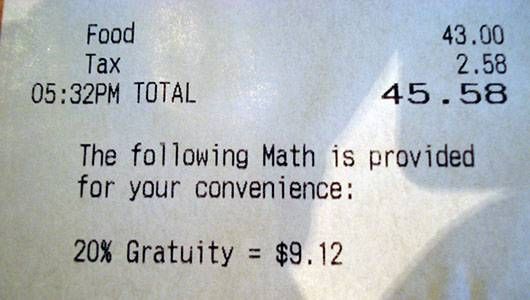

Many restaurants have a policy of charging large groups an automatic service charge. Restaurants that offer on or off-site catering also impose a standard service charge. Every time I see this, I shudder at the tax consequences that await the owners when they are audited.

In almost every case, the service charge is processed through the POS and printed onto the customer’s bill. This is the definition of a controlled tip. This is income of the restaurant. I have yet to see such a bill that charges HST on the automatic gratuity. That would be one sure way to lose a customer. However, HST does apply and the CRA will expect you to pay it, even if you did not actually collect it from the customer.

Most restaurants pay the automatic gratuities to the staff working the event or table. Again, the restaurant must prove the payments, include them on T4s and make required withholdings. Failure to do so will likely result in the deduction of tip payments to employees being disallowed.

I advise my clients to handwrite the gratuity on the customer bill, bypassing the POS system. Handled this way, the “automatic” tips will be indistinguishable from those left by your usual customers.